This post is also available in:

![]()

The data points for this Share of Voice (SoV) study was collected from late May to mid-June, 2025. The results presented below make up and justify the ranking of the top 13 gambling operators in Brazil.

Total operator scores reflect online SoV visibility for casino and sports-related keywords as detected by SEO tools, as well as branded searches, social media presence and estimated organic traffic, in addition to original survey responses.

It should be noted that this is the first Share of Voice study of the year, and that the Brazilian online gambling landscape has undergone massive changes since January 1, 2025. The imposition of the bet.br domain was a key part of the new online gambling regulation, aimed at differentiating operators that meet legal standards.

However, a failure to recognise all bet.br sites as separate domains has severely restricted the organic reach of regulated operators, greatly affecting their visibility. Therefore, operators have faced several challenges in maintaining their online presence.

As a result of this movement, we expect to see considerable shifts in the reported metrics and rankings, as well as an overall decline in search numbers and traffic compared to our last report.

Tracking Popularity on Google Trends

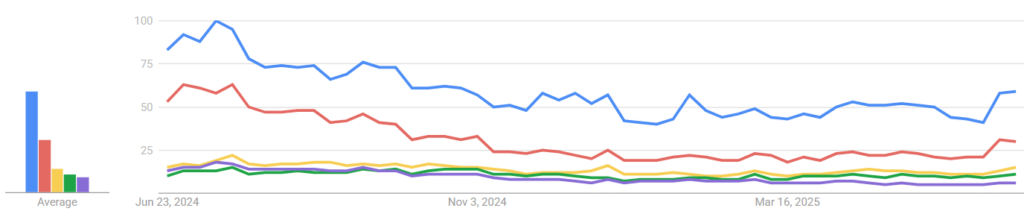

The starting point of our Share of Voice study is the ranking of iGaming operators as they are detected by Google Trends. The graph below shows an estimation of search activity (interest) in the past year, tracked in search terms and not “gaming brands” per se, as recognized by Google Trends.

The top 5 brands’ popularity in the past year, according to Google Trends in late May 2025

As of June 20, 2025, we see the following relative interest in brand-match search queries, compared to the highest possible demand in Brazil in the past 12 months:

| Search Term | Interest via Google Trends | Weighted points assigned to brand |

| 7k | <1 | 0 |

| Bet365 | 31 | 11 |

| Betano | 59 | 20 |

| Betfair | 5 | 2 |

| Betnacional | 11 | 4 |

| Betsson | <1 | 0 |

| Betsul | <1 | 0 |

| Cassino Bet | 1 | 0 |

| EstrelaBet | 6 | 2 |

| KTO | 3 | 1 |

| Novibet | 4 | 1 |

| Sportingbet | 9 | 3 |

| Superbet | 14 | 5 |

Compared to the previous study, Betano remains on top. Moreover, it is the trend setter in terms of peak search interest in the past year, and it keeps gradually widening the gap from its competitors.

Bet365, still second, had its maximum search demand in late 2023 but still maintains consistent brand interest according to Google Trends. While Betnacional maintained its position, the notable is that we added Superbet, who performed better than Sportingbet and took its place in the top 5.

Additionally, four more brands manage to get weighted points – Betfair, EstrelaBet, Novibet and KTO. The remaining brands register marginal interest, weighing at less than 1/20 of the leader.

Gambling Brand Recognition and Trust

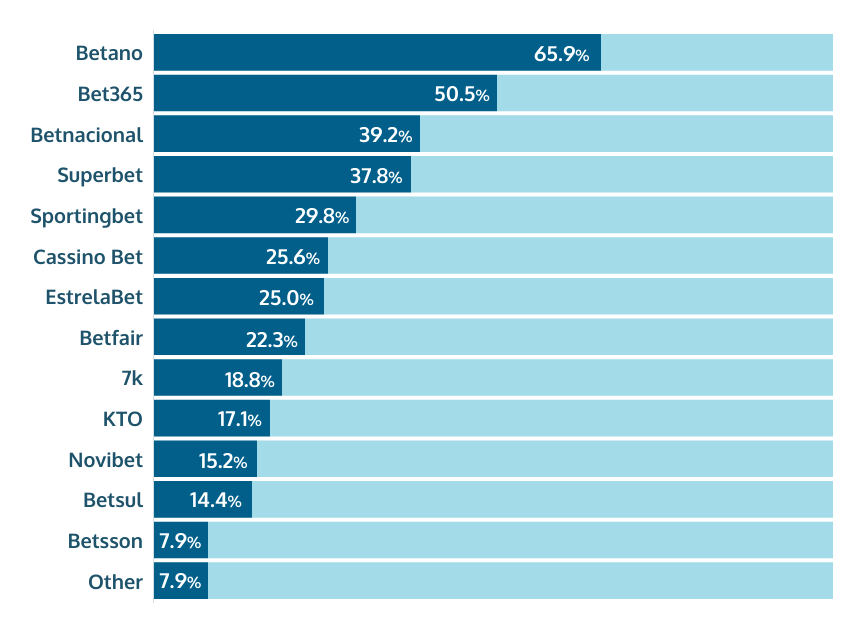

An important variable we need to take a look at is just how well recognized and trusted these online casino and sports betting brands are in Brazil. While based on subjective perception, the ranking below is based on a survey of more than 600 active adult gamblers. We asked them which of the following brands they knew and trusted.

The top 13 standout online gambling websites in Brazil, based on survey responses, were identified in the following order:

To avoid biased replies (response tiredness or overlooking, i.e., temptation to pick early and move ahead), brands appeared in a randomized order to respondents.

As in the previous study, the leaders remain the same: Betano and Bet365. Betnacional has moved up to third place, while Sportingbet has also climbed one position to join the top five. Superbet, a new brand in our studies, received greater recognition, overtaking Sportingbet to claim fourth place. Cassino Bet – another new brand in our study – EstrelaBet and Betfair, were also among the most popular choices in the survey.

This survey selection and resulting ranking attributed additional weighted points to the top 13 gambling brands, which were then added to the final calculation.

| Brand | Recognition and Trust (via survey) | Weighted points assigned to brand |

| Betano | 65.90% | 20 |

| Bet365 | 50.50% | 15 |

| Betnacional | 39.20% | 12 |

| Superbet | 37.80% | 11 |

| Sportingbet | 29.80% | 9 |

| Cassino Bet | 25.60% | 8 |

| EstrelaBet | 25% | 8 |

| Betfair | 22.30% | 7 |

| 7k | 18.80% | 6 |

| KTO | 17.10% | 5 |

| Novibet | 15.20% | 5 |

| Betsul | 14.40% | 4 |

| Betsson | 7.90% | 2 |

| Other | 7.90% | 2 |

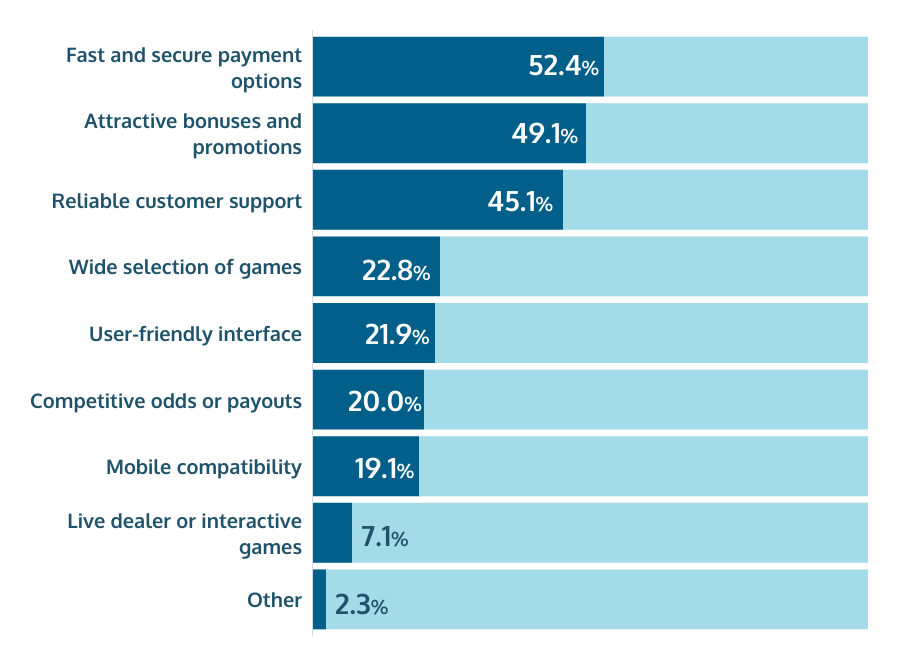

Key Factors for Choosing a Brand

To appreciate what shapes player preferences, we also asked Brazilian players what is most important to them when choosing an online gambling operator. Based on our survey, we saw the following selection:

Unlike in our last study, fast and secure payment options are now at the forefront of the deciding factors for Brazilian iGaming enthusiasts. Attractive bonuses and promotions are also a key preference, with almost half of respondents (49.1%) emphasising their importance.

Reliable customer support (45.1%) remained a key factor for players, maintaining its position from the last survey. In this study, a wide selection of games (22.8%) overtook a user-friendly interface (21.98%), but both are in the top 5.

A seamless, intuitive and well-serviced platform is obviously crucial to players, and these factors ultimately retain consumers, followed by the perception of elevated odds, game returns and high potential payouts attracts players, indicated by the 20%.

Mobile device compatibility is becoming less of an issue nowadays, with only 13.5% of players mentioning it.

The availability of live dealer games is still at the bottom of the above selection (with 4.2%). While immersive and interactive live casino games are engaging and highly sought after by Brazilian audiences, they are not the main reason why players turn to a given brand.

Earlier responses we saw on brand recognition and trust are affected by the list of impact factors we just presented. However, SoV presence is strongly shaped by the likes of paid advertising, online and offline visibility, straightforward fame or notoriety, as well as any recent gaming experiences.

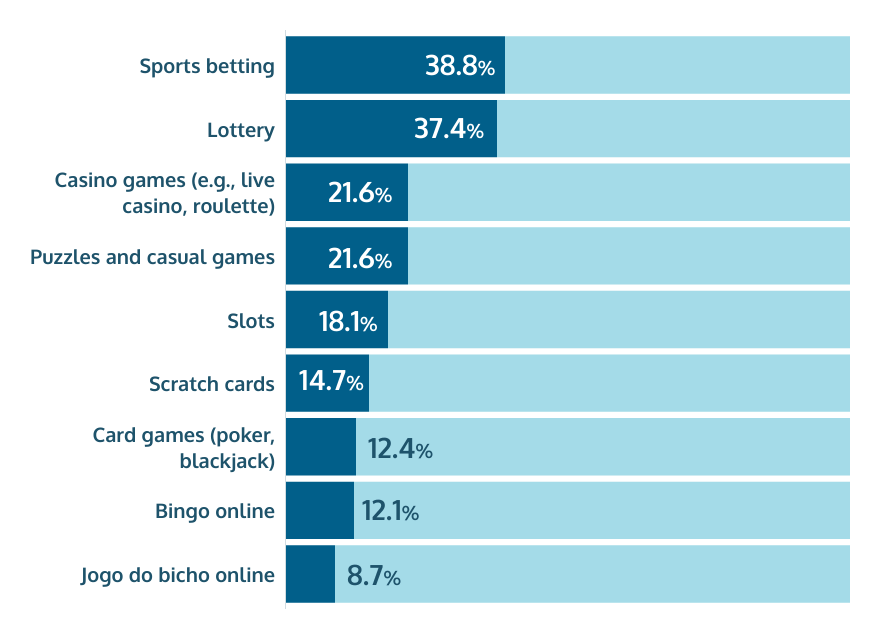

Most Engaging Gaming Verticals

As a next step in our evaluation of generic market shares, we need to analyze the verticals that have the biggest pull among Brazilian real-money gamers.

Sports betting comes in first again, chosen by 38.8% of respondents, with lottery (37.4%) following closely behind.

The fact that gambling has been legal for some time now may encourage more adult respondents to admit taking part in it.. Still, it is remarkable that a traditional form of real-money gaming, such as the public lotteries, is periodically competing with more dynamic and modern gambling products. With that in mind, it is not surprising to see 21.6% of all adult players identify themselves as casino fans.

Another difference from the previous report is that slots dropped to 18.1%, falling behind puzzles and casual games (21.6%) in terms of the most engaging gaming verticals among respondents.

Puzzles and casual games (21.2%) dropped five percentage points, reducing the gap with Jogo do Bicho (20.3%), another traditional Brazilian pastime, which kept its share practically constant.

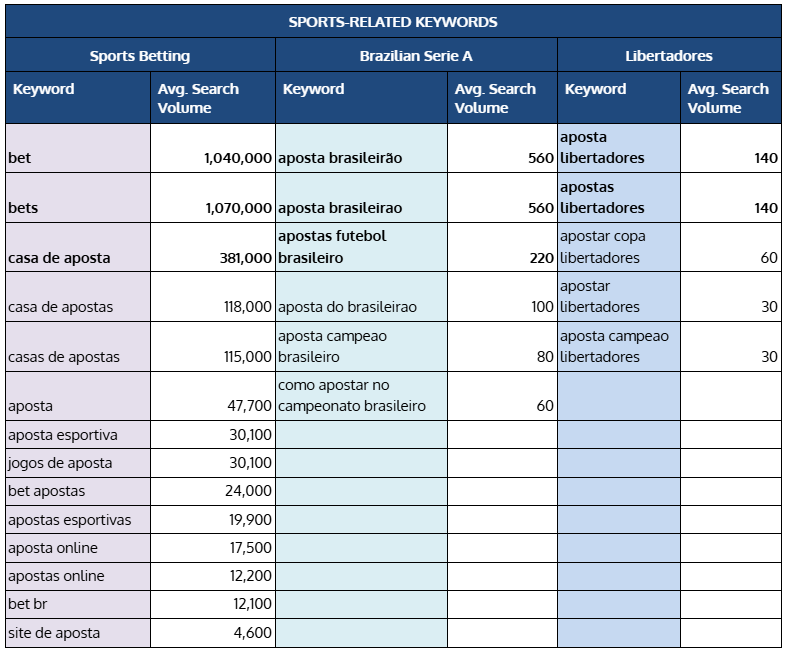

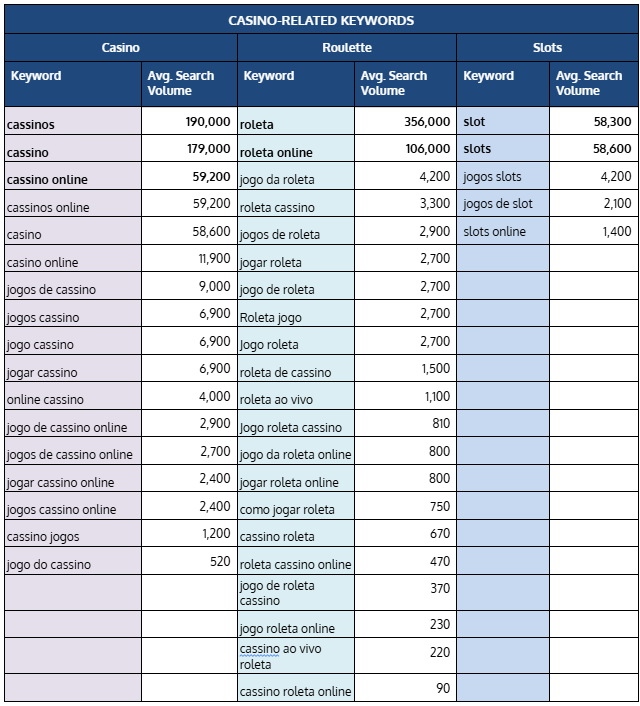

Exploring Online Casino and Sports Search Trends

In this study, we address the two macro-verticals in the igaming industry: online casino and sports betting. We have set out to identify and track the average monthly search volumes of major keywords typical for each vertical. These represent the demand for casino and sports betting gaming products in the last 6 months.

The sports scene is a complex universe in its own right, but when it comes to wagering, we can say that football is the undisputed king of all athletic disciplines. When aggregating sports betting performance of iGaming brands, their Share of Voice will also be reflected in indicators like overall traffic projections and brand mentions, presented further down.

When it comes to the other macro vertical in the real-money gaming industry – online casino – Brazilian casino fans are split between slots and crash games as quick-play options on one hand, as well as live casino games like roulette. And we expect these to get the most mentions and search demand.

It is worth pointing out that since January 1st, changes in regulation have abruptly changed the Brazilian landscape. The transition to a .bet.br domain has been mandatory for all licensed gaming brands and has directly impacted their online presence. As previously stated, we can expect to see a general decline in organic search metrics.

Below, you can see the estimates given by Mangools.com, as of the mid-June, for the average monthly keyword demand in Brazil for the following sports and casino-related terms in the last semester.

As we can see, sports betting terms have a greater presence in terms of volume compared to specific championships and casino-related terms. As previously mentioned, football is a very popular sport in the betting sector, particularly in Brazil, which guarantees higher levels of general interest and, consequently, search volume.

Compared to the previous study, most of the casino-related keywords we tracked recorded stable volumes, though some terms, such as “slots“, saw a significant drop, with average searches falling to 58,600. In terms of growth, there was a slight increase for “cassino”.

The data also suggests that generic, short-tail keywords such as “bet”, “cassino”, “roleta” and “slots” – along with some variations – generate the highest search volumes. This underscores the importance of focusing on basic queries – as much as on branded keywords, if not more – to achieve and maintain consistent online visibility.

On the other hand, specific game searches are more prevalent than undefined game terms, as evidenced by the relatively low search volume for “jogos de cassino” compared to “roleta” and “slot” variations.

Overall Share of Voice Based on Generic Sports-Related Queries

Our breakdown of SoV rankings for various iGaming operators in Brazil is based on a wide range of search queries. For sports-related terms, the overall keyword set consists of over 50 keywords, which are divided into subsets covering a variety of terms and specific queries related to well-known championships.

| Brand | Overall SoV % | Pts | Sports Betting SoV % | Pts | Brazilian Serie A SoV % | Pts | Libertadores SoV % | Pts |

| 7k | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Bet365 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Betano | 0.39 | 1 | 0.32 | 1 | 3.2 | 4 | 5.83 | 4 |

| Betfair | 7.79 | 14 | 11.13 | 20 | 15.47 | 20 | 27.91 | 20 |

| Betnacional | 0 | 0 | 0 | 0 | 0.06 | 0 | 0 | 0 |

| Betsson | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Betsul | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Cassino Bet | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| EstrelaBet | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| KTO | 10.88 | 20 | 10.74 | 19 | 0.99 | 1 | 0 | 0 |

| Novibet | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Sportingbet | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Superbet | 0.02 | 0 | 0.02 | 0 | 0 | 0 | 0.24 | 0 |

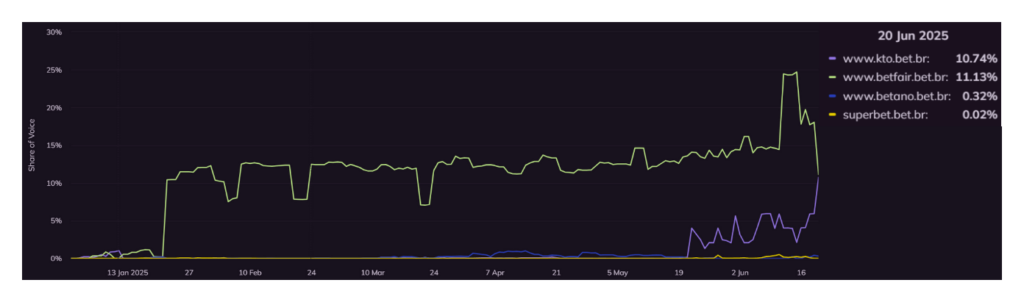

As of 20 June 2025, we have the following shares (and graphs) on Wincher, when we consider all indicators in a single report. This first one covers the Share of Voice in all sports-related searches that we track.

The graphical representation above include all 13 operators we tracked, with compound SoV shares for sports-related keywords that we monitor. (N.B. The screenshots below – for sports-betting, Brazilian Serie A and Libertadores – exclude those brands which show 0% SoV for that niche).

In this matter, two operators have a significant presence. Since late January, KTO has held first place, reaching an impressive 10.88%. Since the start of June, Betfair has been in decline and is now in second place, with 7.79%.

Well behind the top two, we have Betano (0.39%) and Superbet (0.02%). In this vertical, only a few operators are present, with Betfair and KTO capturing most of the visibility and standing out significantly, while the others have little to no presence.

Share of Voice in Sports Betting Queries

A significant similarity can be observed when comparing the overall Share of Voice graphs above and this one. This is because the sports betting subset contains substantially more keywords (14 in total), giving it disproportionate weight in the composition of the overall graph.

Additionally, the words in this group have high semantic coverage and search volume, directly impacting the metric and masking variations from the other groups in the overall graph.

From the operators that reached a percentage of Share a Voice, we have Betfair (11.13%), with a strong performance since late January, despite showing a decrease more recently. KTO has been on an upward trend since mid-June, reaching 10.74%. Betano (0.32%) and Superbet (0.02%) show modest presence.

As explained, it was expected that all the brands would remain practically in the same positions as in the previous graph. However, both graphs still succeed in showing us the presence of these brands in sports-related queries.

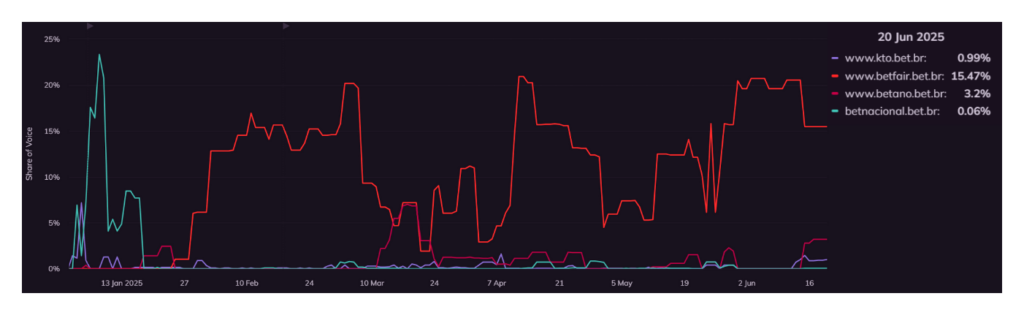

Share of Voice in Brazilian Serie A Queries

.In this subset, we track keywords related to the main national championship, the Brazilian Serie A. Betfair is in first place with a 15.47% Sov and has had little competition over the last six months. Betano (3.2%), KTO (0.99%) and Betnacional (0.06%) have modest shares, while other operators did not perform significantly.

The gap highlights Betfair’s strong presence around the Brazilian Serie A, while the low share of other brands indicates limited visibility within this segment at a national level.

Share of Voice in Copa Libertadores Queries

Copa Libertadores is the most prestigious football championship in South America, and one of the most popular in Brazil, holding a significant share of the national interest.

The list here is even shorter, with Betfair standing out with an incredible 27.91% and once again securing the top position. Betano had a moderate presence with 5.83%, and finally, there is Superbet with 0.24%.

For the sports vertical, we see that Betfair has a dominant position, while the other operators struggle to maintain a consistent competitive presence in organic results over time.

Overall Share of Voice Based on Generic Casino-Related Queries

As in our sports-related analysis, we have a breakdown of SoV rankings for various iGaming operators in Brazil, based on a wide range of casino-related search queries, including 45 keywords from essential game categories – namely slots, roulette and general casino terms – listed above.

| Brand | Overall SoV % | Pts | Cassino SoV % | Pts | Roleta SoV % | Pts | Slots SoV % | Pts |

| 7k | 0.01 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Bet365 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Betano | 1.65 | 6 | 5.02 | 10 | 1.38 | 20 | 0.68 | 7 |

| Betfair | 2.66 | 10 | 10.02 | 20 | 1.1 | 16 | 0.45 | 5 |

| Betnacional | 0.09 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Betsson | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Betsul | 0.04 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Cassino Bet | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| EstrelaBet | 0.01 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| KTO | 5.36 | 20 | 8.43 | 17 | 0.21 | 3 | 1.97 | 20 |

| Novibet | 0.04 | 0 | 0.03 | 0 | 0 | 0 | 0.52 | 5 |

| Sportingbet | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Superbet | 0.05 | 0 | 0.07 | 0 | 0 | 0 | 0 | 0 |

As of 20 June 2025, we have the following shares (and graphs) on Wincher, when we consider all indicators in a single report.

The graphical representation above, taken from Wincher.com, includes all 13 operators we tracked, with compound SoV shares for all casino-related keywords that we monitor. (N.B. The screenshots below – for casino, roulette and slots – exclude those brands which show 0% SoV for that niche).

Since April, Betnacional and KTO have been competing for first place, but Betnacional saw a drop in the last few days of May. KTO (5.36%) is at the top among online gambling operators in Brazil, based on all query terms included. Betfair (2.66%) increased at the beginning of June, taking second place.

Betano (1.65%) has been improving in June, moving up to third position. Betnacional (0.09%) and Superbet (0.05%) complete the top 5, but they are a long way behind the top 3.

Worth pointing out is the fact that many of the underperforming brands in online environments make up their market shares with land-based promotions and coverage. Others post lower than expected metrics because of a JavaScript-based SEO and content rendering – with bet365 a prominent example.

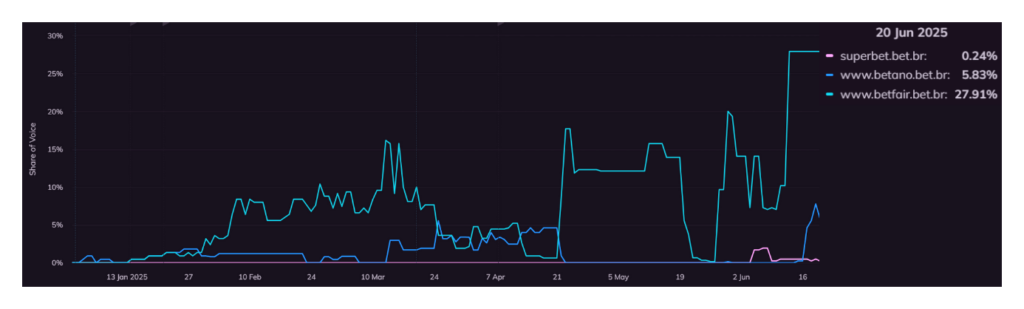

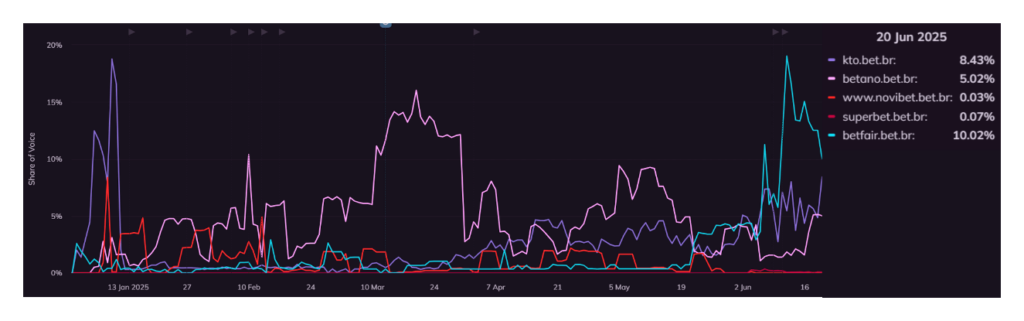

Share of Voice in Casino Specific Queries

For casino-related searches in particular, Betfair (10.02%) and KTO (8.43%) posted significant growth in the first few days of June, securing first and second place respectively. Betano declined in mid-May but still made it to third position with 5.02%. Once again, the top 3 are well ahead of their competitors.

Novibet experienced some ups and downs, but managed to have a presence, as well as Superbet (0.07%).

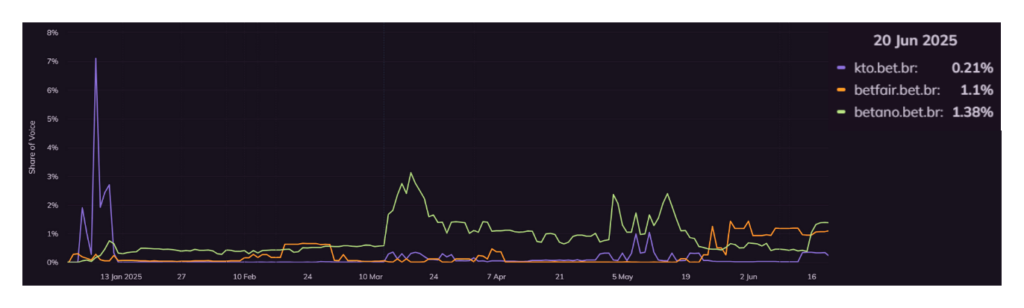

Share of Voice in Roulette Queries

Looking at roulette-related queries, we only see the shares of a few competitors and they are closer to one another. It appears increasingly hard for most brands to have an impact and emerge in terms of online visibility for roulette searches, as almost all operators drop shares in absolute terms.

Betano takes the top position, growing from 0.2% to 1.38%. Betfair follows in second place, dropping from 1.91% to 1.1%, but still making the top 3. Meanwhile, KTO dropped from 0.46% to 0.21%, maintaining the same position from last study,

Besides being a casino classic, online roulette remains one of the most sought-after gaming products on a global level, particularly in its live casino version. High levels of online demand make it a difficult vertical to compete for, and that is why we are not surprised to see the small presence of online gambling operators.

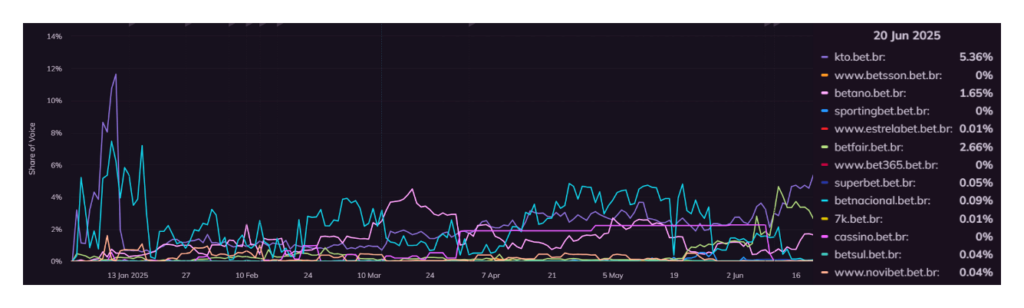

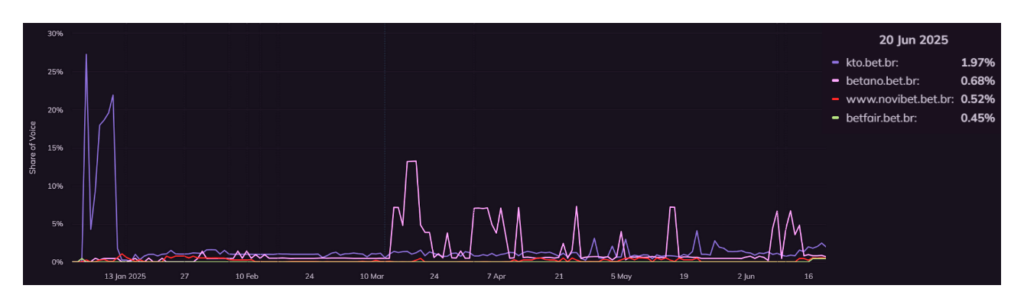

Share of Voice in Slot Queries

When it comes to slot-related queries, KTO (1.97%) has more than twice the share of its nearest competitor, Betano (0.68%), which has maintained its position since the last study. Third place goes to Novibet, which dropped from 0.67% to 0.52%.

Betfair’s share decreased from 0.56% to 0.45% since our previous study, but it still managed to maintain a presence. None of the other operators had an online slot SoV presence.

The online slots niche is possibly one of the most dynamic segments in real-money gaming. Tens of thousands of games are already on the market and hundreds come out each week. Being able to maintain high levels of online visibility and market recognition requires coordinated efforts in SEO, product delivery and superior player support.

It is important to keep in mind that slot-related queries in Brazil include both “slot” and “caça niqueis” keywords. This is the only keyword category that uses both the English and Brazilian terminology for the game, so operators with SEO efforts in both will have a clear advantage here.

Moreover, effective SEO depends on precise targeting of specific titles, as noted above. Operators also face daily challenges with social media trends and naming customs (nicknames for games and characters).

Working with SEO

When analysing keyword rankings, we saw a significant difference between the operators. Only a few brands performed well in this area, while the majority had very low or non-existent results. This difference can be attributed to the active efforts in search engine optimization and investment in SEO strategies.

Another factor that may have had a negative impact on the performance of these brands, especially in the first few months of the year, was the legal changes in Brazil, with the introduction of bet.br domains. Even so, the narrow focus on SEO initiatives is a major factor behind the performances.

Despite this, the study’s methodology remains consistent, including highly renowned operators. The lack of scores for some brands reflects what we see in terms of SEO in today’s market, where only a smaller group of operators actually demonstrate competitiveness in this channel.

Evaluating Brand Awareness via Monthly Search Volumes

In our quest to weigh brand recognition among iGaming operators in Brazil, we analyzed brand-specific online queries for some of the leading gaming platforms. The ranking below encompasses some of the most recognized brands locally, providing a snapshot of their market presence.

It is important to keep in mind that the total figures do not mean unique users; they include recurring searches by the same users finding the page through Google Brazil (as estimated by Mangools).

We indicate only the volume of exact branded queries, excluding misspellings or potentially related keyword combinations.

| Brand | Monthly Searches | Change in Search Volume | Pts |

| 7k | 161,000 | n/a | 0 |

| Bet365 | 21,200,000 | -66.3% | 9 |

| Betano | 45,800,000 | -1.5% | 20 |

| Betfair | 2,440,000 | -76.1% | 1 |

| Betnacional | 10,400,000 | -12.6% | 5 |

| Betsson | 36,600 | -55.5% | 0 |

| Betsul | 279,000 | +20.7% | 0 |

| Cassino Bet | 105,000 | n/a | 0 |

| EstrelaBet | 5,000,000 | -18.0% | 2 |

| KTO | 1,740,000 | -20.9% | 1 |

| Novibet | 2,670,000 | -1.1% | 1 |

| Sportingbet | 7,750,000 | -14.8% | 3 |

| Superbet | 11,100,000 | n/a | 5 |

For this semester, Betano takes first place as the most searched brand in Brazil, with over 45 million monthly searches. Bet365 is in second place, despite a significant drop of 66.3% since the last study. Superbet and Betnacional are close behind, securing good positions.

The mid-ranking operators include Sportingbet (7.75 mln), EstrelaBet (5 mln), Novibet (2.67 mln), Betfair (2.4 mln) and KTO (1.74 mln). The remaining operators did not register more than 300,000 monthly searches.

With the exception of Betsul, which saw an increase, all the operators experienced a drop in searches, some more than others. Betfair (-76.1%), Bet365 (-66.3%) and Betsson (-55.5%) were most affected by the general decline in monthly searches.

Casinos’ Monthly Traffic Estimates

An important part of our study is the monitoring of the estimated monthly organic traffic that these competitors receive from Brazil (only). We utilize proven and trusted SEO analytic tools provided by Ahrefs and Semrush.

| Brand | Monthly Organic Traffic (via Ahrefs) | Monthly Organic Traffic (via Semrush) | Average traffic (est.) | Percentage Change | Pts |

| 7k | 3,600,000 | 929,700 | 2,264,850 | n/a | 2 |

| Bet365 | 294,000 | 339,199 | 316,600 | -97.8 | 0 |

| Betano | 13,700,000 | 32,700,000 | 23,200,000 | +23.1 | 20 |

| Betfair | 2,000,000 | 2,700,000 | 2,350,000 | -7.8 | 2 |

| Betnacional | 7,100,000 | 2,800,000 | 4,950,000 | -22.7 | 4 |

| Betsson | 1,800 | 3,133 | 2,467 | -98.8 | 0 |

| Betsul | 154,000 | 219,286 | 186,643 | +14.1 | 0 |

| Cassino Bet | 513,000 | 576,025 | 544,513 | n/a | 0 |

| EstrelaBet | 1,600,000 | 2,900,000 | 2,250,000 | -11.8 | 2 |

| KTO | 1,100,000 | 1,300,000 | 1,200,000 | -40.0 | 1 |

| Novibet | 1,700,000 | 2,000,000 | 1,850,000 | +37.0 | 2 |

| Sportingbet | 2,900,000 | 7,800,000 | 5,350,000 | -10.1 | 5 |

| Superbet | 4,900,000 | 2,900,000 | 3,900,000 | n/a | 3 |

Since the estimates for organic traffic differ greatly in some cases, we consider the mean (average) value when ranking the website traffic and, consequently, assigning the weighted points for that indicator. We also have the percentage change based on the previous study.

With a 37% increase, Novibet was the biggest gainer for the reporting period, but Betano remained in first position, having increased its average traffic by 23.1%. Meanwhile, Sportingbet is performing strongly in second place.

Betnacional is now one of the top 5 gambling brands in Brazil by organic traffic, along with Superbet and 7K.

Bandwagon Effect Implications

The bandwagon effect is a phenomenon where individuals tend to align with popular choices. This is especially common in the absence of in-depth expertise and plays a significant role in brand recognition.

In the iGaming sector, such behavior would suggest that the most recognizable operators, or those perceived as leaders, are more likely to be chosen by consumers. However, it is interesting to note that while some operators may be more recognizable in reality, they might not always be the top choices or at least not by such a wide margin.

Why Do Players Switch? Frequency and Motivations for Choosing a New Online Casino or Sportsbook

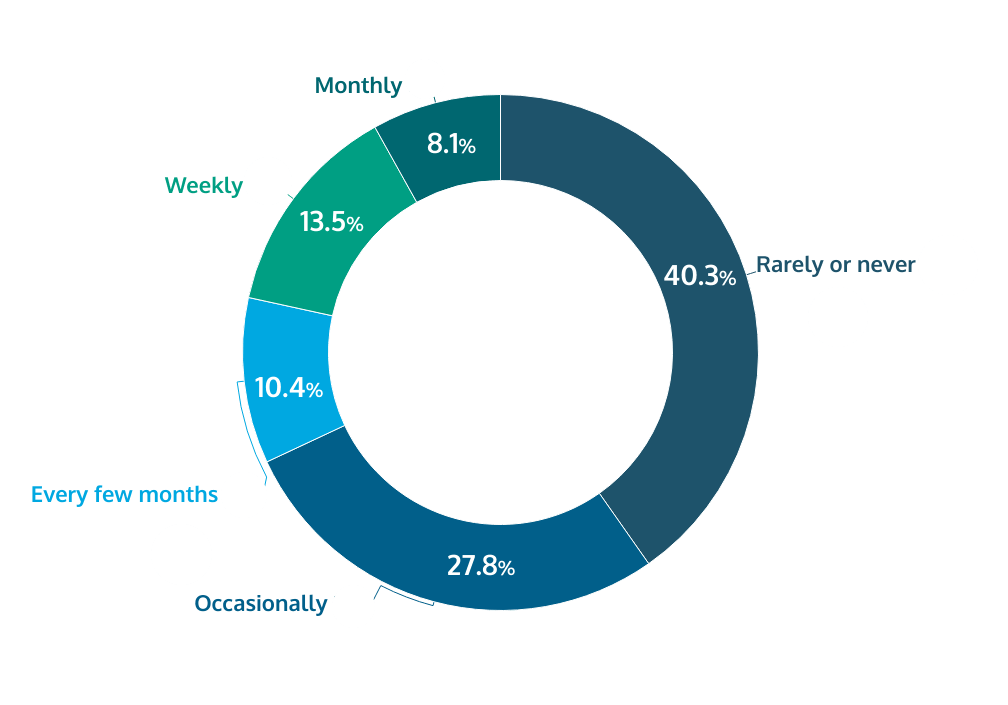

Our survey also reveals the consistency and loyalty of player engagement with leading iGaming operators. The largest share of respondents (40.3%) rarely or never switch between different iGaming operators, suggesting a state of brand loyalty development. Combined with those that only occasionally switch (27.8%), we have more than two-thirds of players who have a largely routine pattern on gaming.

Additionally, more than 20% of all players switch operators at regular intervals – 8.1% do so monthly, and 13.5% weekly. This highlights a group actively seeking new gaming experiences and promotions.

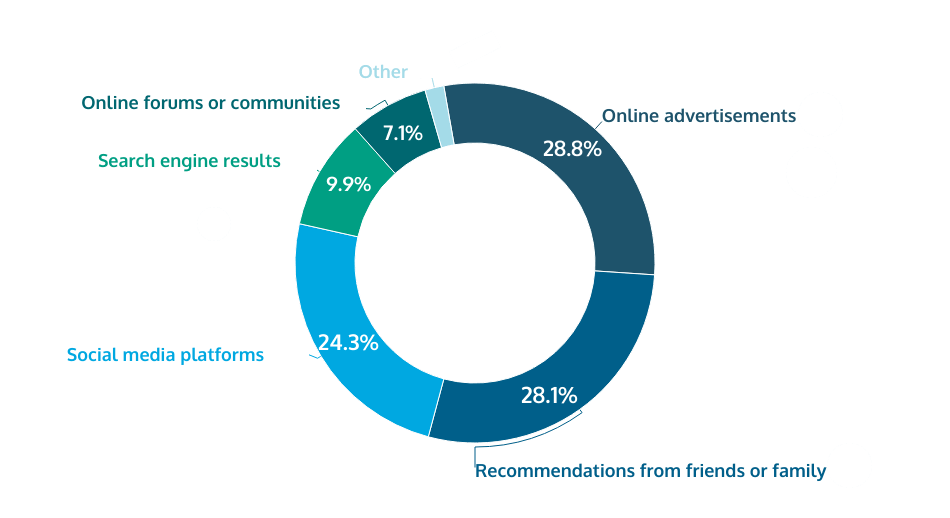

Discovery Channels for New Gaming Platforms

When it comes to discovering new iGaming sites or apps, online advertisements have become the primary method for 28.8% of respondents. Combined with the 24.3% attributed to social media platforms, it underscores the effectiveness of digital marketing strategies in the industry.

Although social media have dropped in position compared to the last report, they are still one of the main channels for discovering new platforms. This indicates that real-money gaming has become a more natural part of daily life and entertainment for its fans.

The high impact of personal recommendations (28.1%) is always expected and the perception of community gaming is complemented by the 7.7% attributed to online forums. On the other hand, the fact that search engine results have shown some increase, being cited by 9.9%, suggests that players are actively looking for their own channels of information and discovery.

Reasons for Switching – Non-Gaming Factors and Desired Improvements

As we noticed, there are a number of factors that influence the choice of an iGaming platform, many of which lay outside of those directly related to one’s gaming experience.

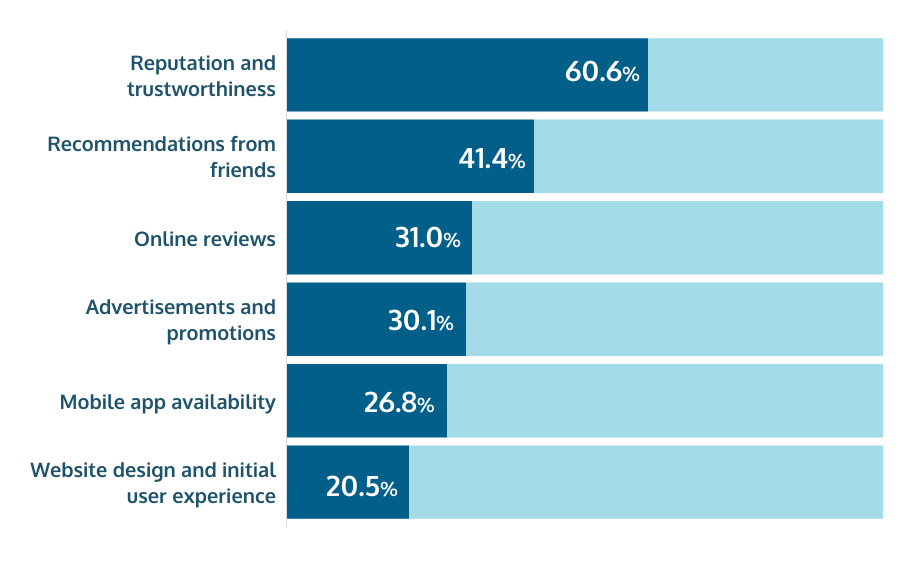

Reputation and perceived trustworthiness are the most influential non-gaming factors, with 60.6% of respondents. In other words, trust and credibility in the iGaming industry goes a long way for most users.

Recommendations from friends (41.4%) maintain their importance and are always decisive, as are online reviews (31%) and promotions (30.1%). In terms of experience, the availability of mobile apps (and therefore compatibility) and website design and UX maintained their positions, with 26.8% and 20.5% respectively.

Even when some key features are not decisive for gamers, many are eager to see improvements in certain areas.

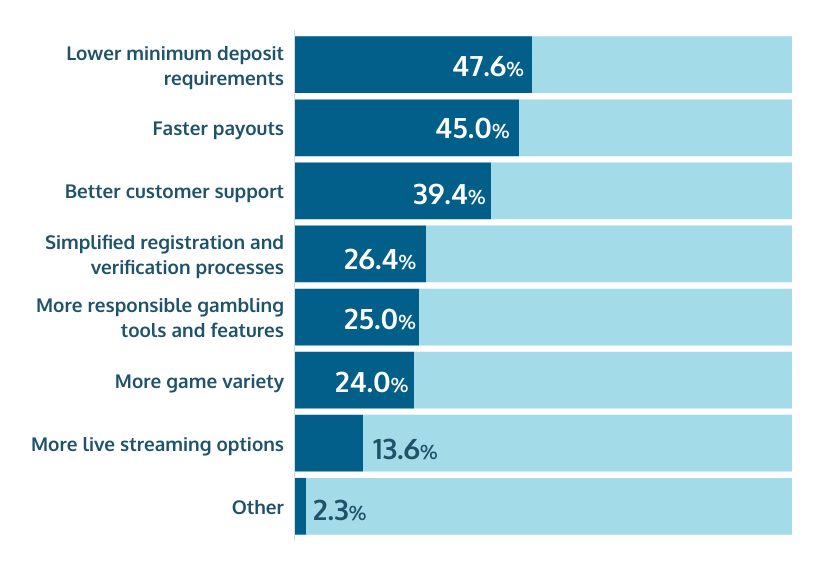

There has been a significant change in the ranking of desired improvements. Lower minimum deposit requirements (47.6%) now tops the list, replacing faster payouts (45%), which had the most respondents in the last two studies.

Better customer support (40%) is among the most important factors for respondents, followed by a simplified registration and verification process with 36.8%. This indicates the gamer expectations of a smooth and trouble-free user journey, from registration to reliable support.

Responsibility is also a factor for a quarter of all gamers, those that picked “more responsible gambling tools and features” (25%). These factors increasingly point to the need for better accessibility, but in a safe and responsible manner – all features of a maturing market, once again.

Gaming Brand Followers on Major Social Media Networks in Brazil

Last but not least, our analysis needs to factor in the importance of Social Media followers in Brazil. The table below shows the adherence of users to these channels. Again, we only consider dedicated Brazilian accounts for the iGaming brands in the study.

| Brand | Instagram followers | X followers | Facebook followers | Total | % Change | Pts |

| 7k | 1,100,000 | 2,232 | n/a | 1,102,232 | n/a | 18 |

| Bet365 | n/a | n/a | n/a | n/a | n/a | 0 |

| Betano | 558,000 | 72,300 | 92,000 | 722,300 | + 19.4 | 12 |

| Betfair | 229,000 | 162,600 | 12,000 | 403,600 | +7.9 | 7 |

| Betnacional | 365,000 | 12,200 | 28,000 | 405,200 | +87.6 | 7 |

| Betsson | 20,900 | 4,146 | 42,000 | 67,046 | -0.1 | 1 |

| Betsul | 93,400 | 3,995 | n/a | 97,395 | +28.0 | 2 |

| Cassino Bet | 1,200,000 | 1,381 | 13,000 | 1,214,381 | n/a | 20 |

| EstrelaBet | 919,000 | 23,400 | 17,000 | 959,400 | +10.8 | 16 |

| KTO | 210,000 | 38,900 | n/a | 248,900 | +6.7 | 4 |

| Novibet | 40,800 | 2,722 | 2,900 | 46,422 | +36.9 | 1 |

| Sportingbet | 291,000 | 17,100 | 267,000 | 575,100 | +25.6 | 9 |

| Superbet | 265,000 | 31,000 | 6,700 | 302,700 | n/a | 5 |

N.B. Bet365 does not have dedicated Social Media profiles for the Brazilian market at the time of writing.

Unsurprisingly, Instagram is the most popular social media platform where iGaming operators create and maintain an account. As in the previous study, Facebook is in second place and Twitter is the third most popular social media network among iGaming profiles.

Facebook is still big in Brazil and seems to be slightly gaining ground in gaming. Despite that, we consider the followers in a cumulative count, even if many of these might be overlapping and registered across more than one Social Media platform.

Cassino Bet proves its powerful outreach on social media, dominating in total followers and extending its lead over its competitors. 7k comes second, while EstrelaBet is now in third place on the podium, posting a modest growth. This time, the top 5 is completed by Betano, who remains in fourth place, and Sportingbet, with a 26.6% increase in the number of followers.

Final Evaluation on iGaming Operator “Share of Voice” Rankings in Brazil

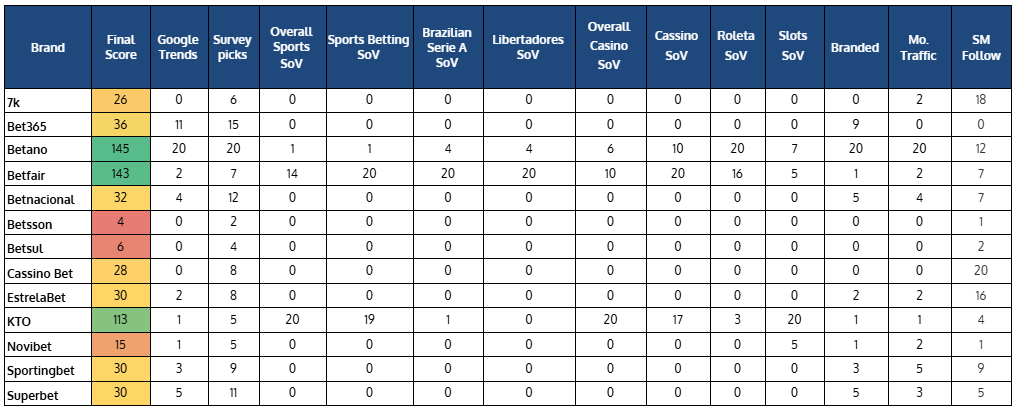

Most of the operator metrics complement the survey responses we analyzed earlier, point in the same direction or act an extra dimension when painting the complete picture of the online visibility of the top 13 gambling brands in Brazil. This allows us to combine these sources and rank the most popular online gaming operators in the country.

The table above contains the combined rankings of the iGaming operators in Brazil, showing the separate categories side by side. Based on the above methodology, we can see how these brands rate against one another.

However, the way our points system ranks them, we do not perceive an estimation of the market shares and online Share of Voice of these gambling brands in their most pragmatic expression – percentages.

With the due conditional provisions, we can provide a solution based on the average monthly estimated traffic (see above). The latter adds up to around 68.2 million organic visits for all brands in our study. Earlier ENV Media research had shown that – out of just about 100 million adult real-money gamers in Brazil – most play “occasionally throughout the year” or approximately “once a month”.

Such levels of real-money gaming frequency combine for 61%, taking the median value reasonably close to “once a month”. This would see the resulting gaming activity correspond closely with the concept of unique monthly visitors.

Therefore, it is reasonable to accept that the above top 13 operators – their online traffic, visibility and weighted points as assigned in our study – cover a comparable total combined share of the market, 68.2%.

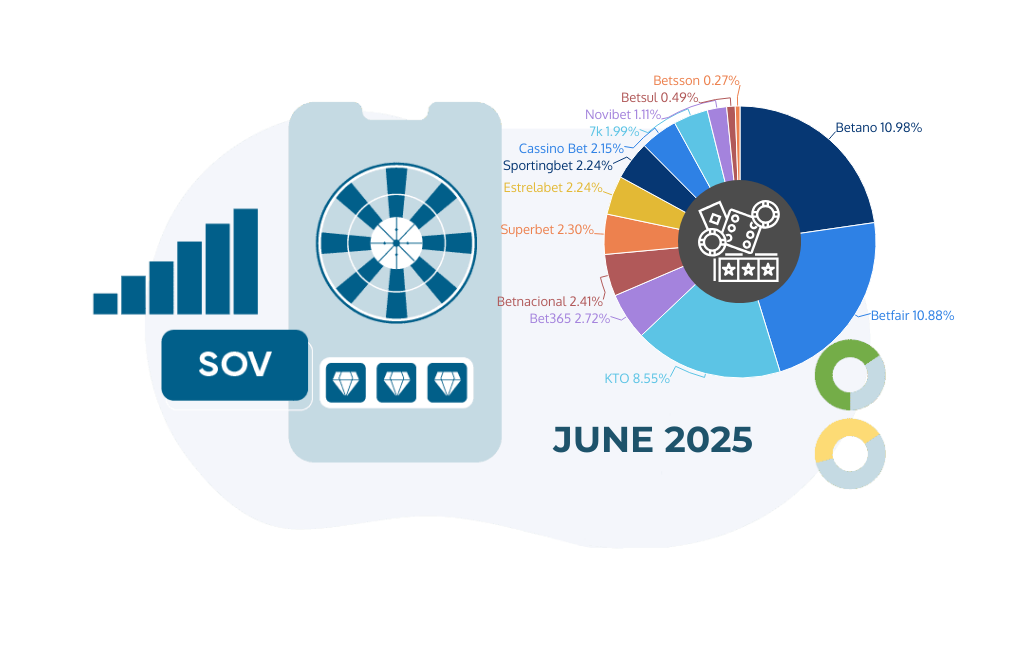

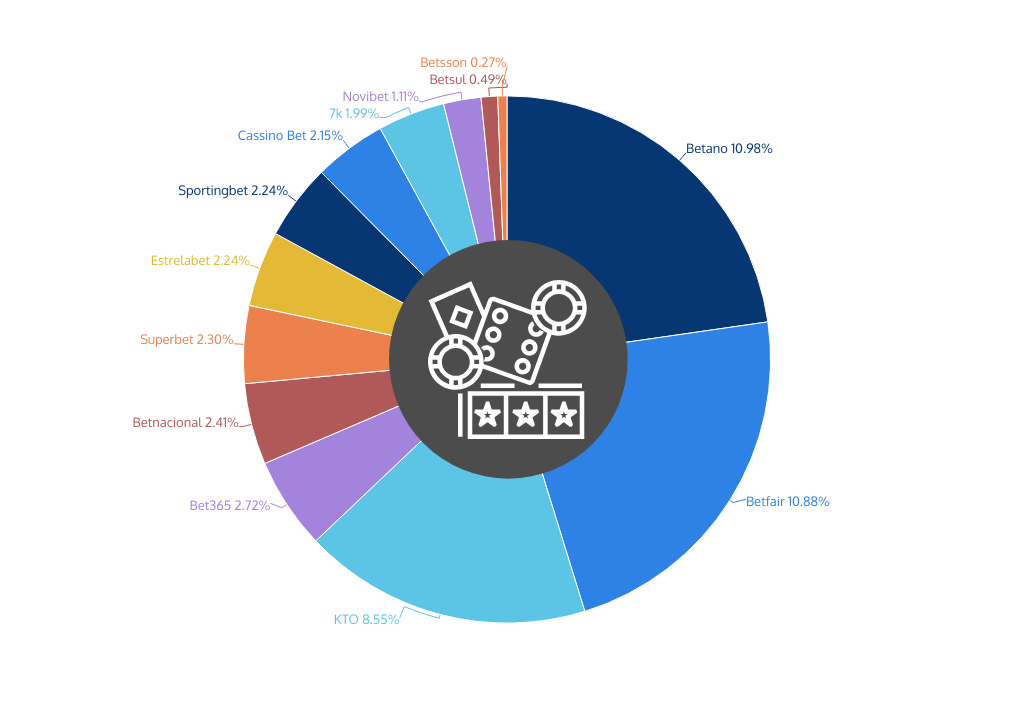

Our systematic approach leads us to conclude that the Share of Voice of the top 13 iGaming operators in Brazil is reasonably well represented (in market share percentages) by the table below:

| Brand | Est. Online Market Share | % Change |

| Betano | 10.98 % | +6.1 |

| Betfair | 10.88 % | +21.8 |

| KTO | 8.55 % | +28.7 |

| Bet365 | 2.72 % | -62.7 |

| Betnacional | 2.41 % | -26.2 |

| Superbet | 2.30 % | n/a |

| Estrelabet | 2.24 % | -14.0 |

| Sportingbet | 2.24 % | -31.5 |

| Cassino Bet | 2.15 % | n/a |

| 7k | 1.99 % | n/a |

| Novibet | 1.11 % | -62.2 |

| Betsul | 0.49 % | -36.0 |

| Betsson | 0.27 % | -81.2 |

N.B. This methodology naturally excludes users who play across multiple platforms, creating overlapping market shares.

Ultimately, standout operators like Betano and Betfair confirm their dominant performance in terms of Share of Voice (SoV) and overall digital market presence. Based on our weighted points system, we can objectively assess the top 13 online gaming operators in Brazil in terms of their online traction – especially relative to their competitors – and effectively highlight their strengths and weaknesses.

There are a couple of significant changes we need to analyze when comparing the results to our last report. The first one sees KTO take the third spot in estimated market share in Brazil, standing out in terms of growth (+28.7%). Bet365, which previously occupied the podium, saw a 62.7% drop in market share and now ranks fourth, followed by Betnacional.

Another significant difference from last time is the large gap between the top 3 operators and the others. As previously mentioned, we expected significant changes and a general decline in metrics due to the imposition of the bet.br domain. This, coupled with the active SEO efforts of these brands, explains the large percentage difference between the top 3 operators and the others. Still, it is clear that the popularity of leading iGaming verticals such as sports betting and casino games define the digital gambling landscape of Brazil.

Ultimately, the above findings illustrate the profound impact of targeted SEO strategies. Operators with optimized content and superior digital marketing practices rank higher in search engine results and enjoy enhanced visibility and organic traffic. While recent domain shifts may cause short-term disruption, consistent SEO work remains one of the most effective ways to build and maintain a strong presence in an increasingly competitive iGaming landscape.